A Message from the Chancellor

On Oct. 24, 2023, Chancellor Gilliam shared a message with faculty and staff regarding the University’s finances. To read the message, click here. Below you will see the supporting slides of accurate University budget information refuting the primary conclusions in the AAUP report. University financial operations are complex, but our challenge boils down to this: we are bringing in fewer of the kinds of dollars we can use for academic programs.

1 of 7

Over 85% of the University’s budget is dependent on enrollment. This slide includes headcount and student credit hours (which state appropriations are based on). As you can see, as measured by headcount, FTE, and SCH, overall enrollment is down significantly. As the second table shows, the University has increased faculty personnel during this enrollment decline while other units, including administrative, have decreased personnel.

2 of 7

This data shows graduate and undergraduate trends since 2018. Note that we are projecting declines in graduate enrollment and accounting for continuing cohort drag from smaller incoming classes in 2021 and 2022. We expect small gains in undergraduate enrollment in the coming years, but not enough to make up for the cohort drag and graduate enrollment declines. In addition, all demographic projections are that there will be fewer available undergraduates both in the U.S. and North Carolina after 2025. An enrollment rebound is not likely, and we must adjust.

3 of 7

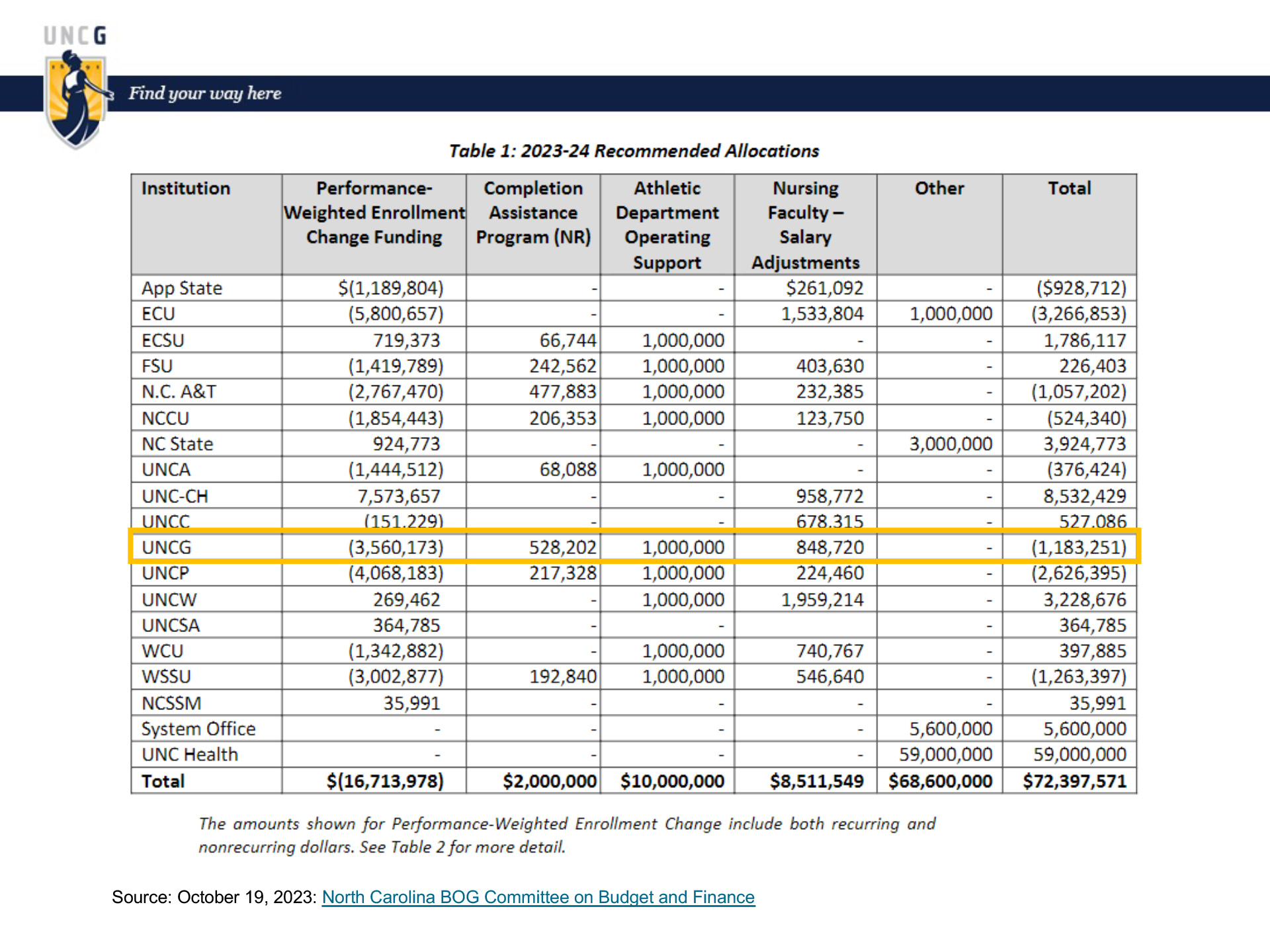

The AAUP report claims that UNCG does better under the new funding model. This is false. This slide from the UNC System Office shows how each campus fares under the new model. Note, UNCG is down $8m under the new model compared to last year (and gains $2.3m in performance weighting). Also of note, in December 2022, the Chancellor went before the Board of Governors and asked for a special “stop gap” measure of $2.3m to help UNCG adjust to the change in the new funding formula. It was granted but was told not to come before the Board again with another such request. The Chancellor wouldn’t have requested, nor the Board of Governors granted this special accommodation, if we had the unlimited resources the AAUP report claims the University has.

4 of 7

This slide shows our additional non-capital appropriations from the Legislature, but even with these additional appropriations we are still to the negative.

5 of 7

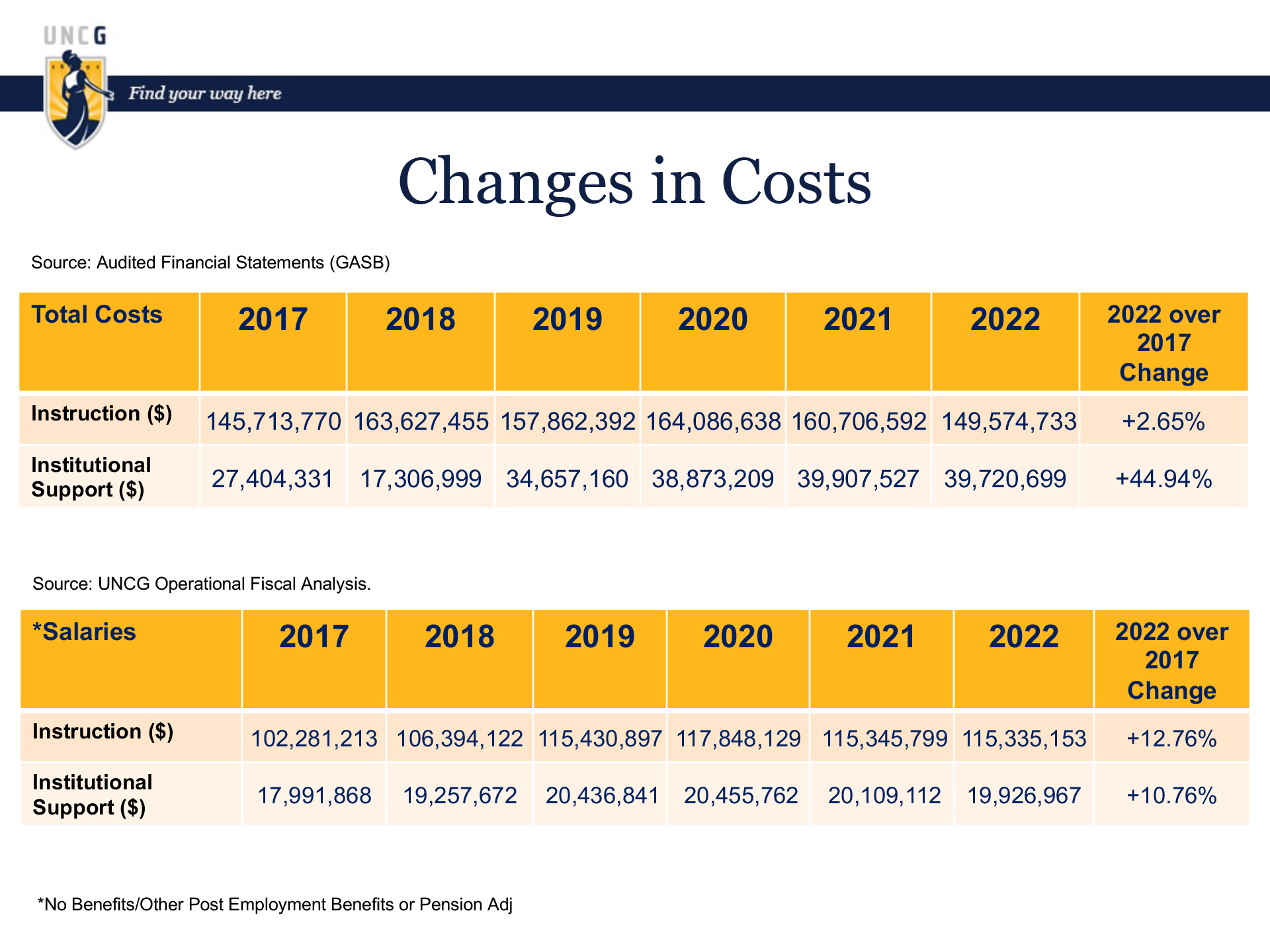

The top table is AAUP/Bunsis information. Financial statements are aggregate, presenting general financial information in a manner that can be read by multiple audiences. For instance, this budget category includes significant post-employment (retirement) benefits (labeled OPEB in the financial statement). This failure to disaggregate the data is the source of Bunsis’s egregiously mistaken claim that the university is disproportionately spending on administration over instruction. The bottom table disaggregates the instructional and institutional costs, reconciled to the audited financial statement, excluding benefits, HEERF and nonwage items, which translates to what was spent on salaries. As you can see, what we spent on instructional salaries (in the aggregate) outpaced slightly institutional support salaries.

6 of 7

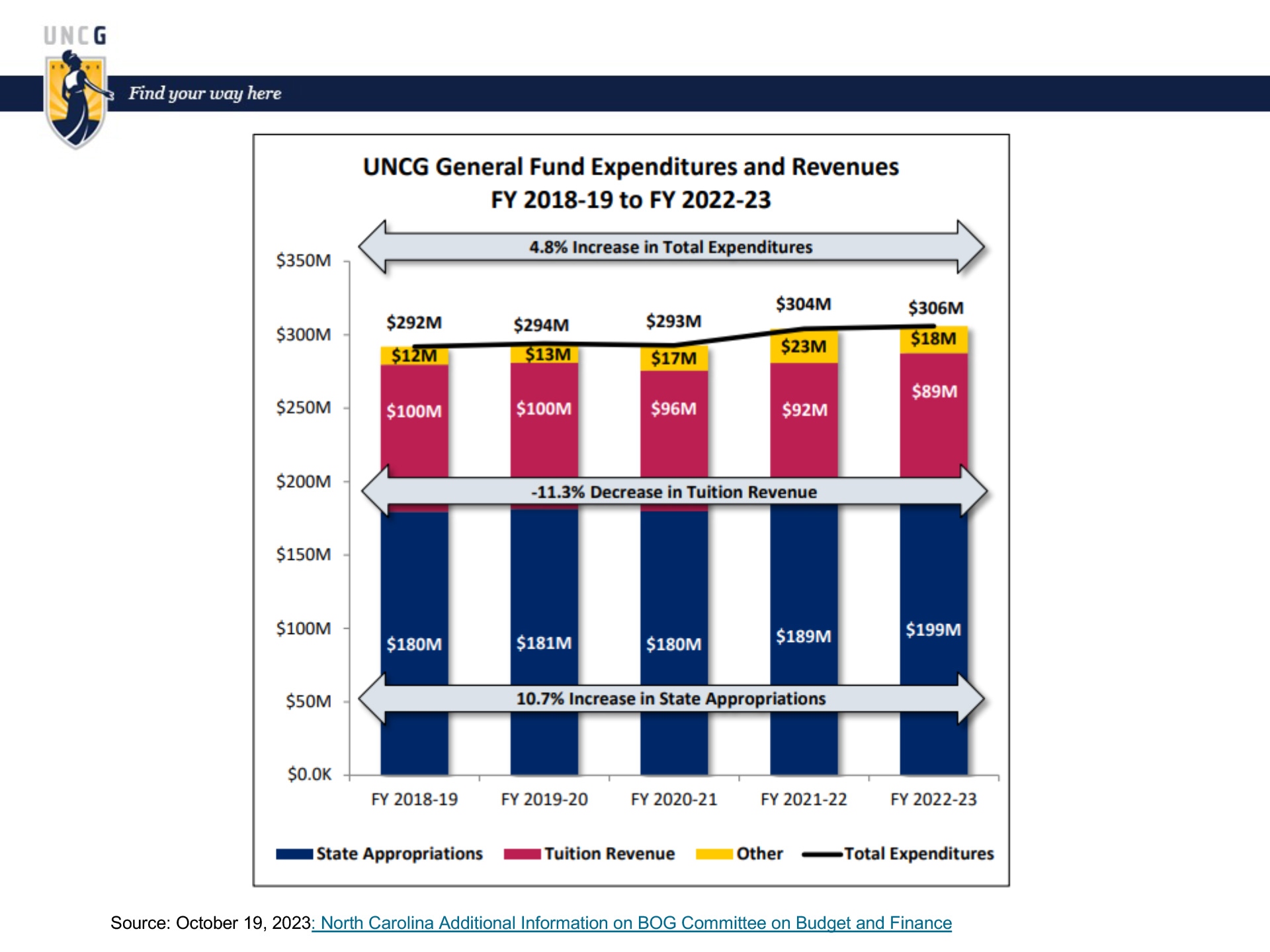

These data show the increase in total expenditure and decrease in tuition revenue. Note that the state appropriations increases are largely due to legislative salary increases for employees (essentially a pass through in our budget) and specific projects (e.g., Jackson Library, Chiller Plant, Steam Plant, other repairs and renovations).

7 of 7

The AAUP report also recommends that we cut athletics spending. Bunsis claims that the University redirects spending from academics to athletics to the tune of $4.5 million dollars. Athletics is funded primarily by the student athletics fee (approximately 85% of their budget), which cannot be used for other purposes. Hypothetically even if we eliminated this athletic student fee (or athletics department for that matter), we would not be able to repurpose the fee. In addition, athletics is also funded by philanthropy, NCAA contributions, and small contributions from ticket revenue and concessions. There was a one-time allocation of $990K in funding from federal HEERF (Higher Education Emergency Relief Funds) dollars, $379,000 from a Pepsi contract, and a small contribution from the Chancellor’s fund ($75k). The NCAA requires us to calculate indirect costs to support Athletics, much like we do when determining our overhead rate for grants and contracts. This includes in-kind salaries from human resources, IT, finance and administration, and other areas. These are not fund allocations distributed to Athletics (as the AAUP report would have you believe), but instead, a calculation of how much time is devoted from various areas in the institution to support Athletics.